{kind=link}

CA. Vikram Garg

Section 43B(h) of Income Tax Act, 1961 has become a hot topic of discussion between the businessmen and tax professionals. Among the plethora of legal compliances, insertion of clause (h) to section 43B of Income Tax Act,1961 vide finance bill 2023 applicable from the financial year 2023-2024 onwards has supplemented to the woes.

The section provides that any sum payable by a buyer to a micro or small enterprise beyond the time limit specified under the Micro, Small and Medium Enterprises Development Act, 2006 (MSMED, Act 2006) shall be allowed as expenditure in the financial year in which sum is actually paid and not in the year when such a liability is incurred irrespective of the method of accounting being followed.

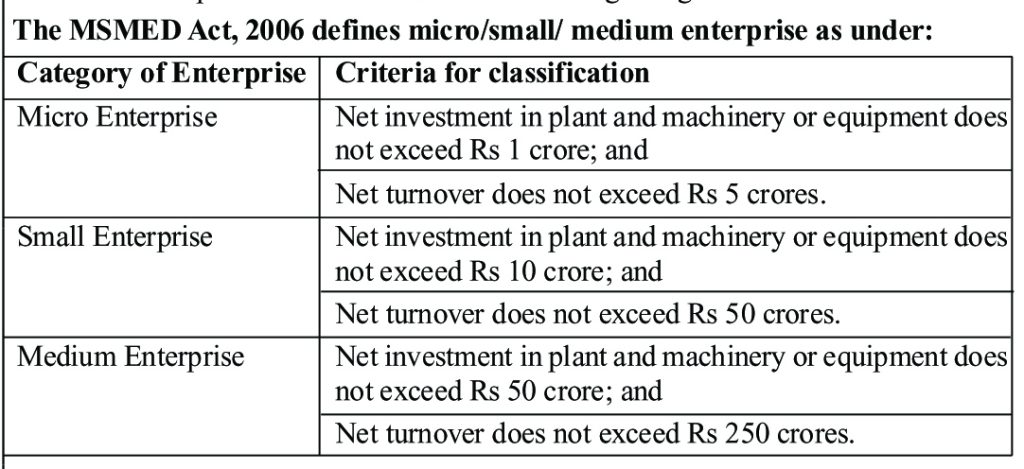

The MSMED Act, 2006 defines micro/small/ medium enterprise as under:

Category of Enterprise Criteria for classification

Micro Enterprise Net investment in plant and machinery or equipment does not exceed Rs 1 crore; and

Net turnover does not exceed Rs 5 crores.

Small Enterprise Net investment in plant and machinery or equipment does not exceed Rs 10 crore; and

Net turnover does not exceed Rs 50 crores.

Medium Enterprise Net investment in plant and machinery or equipment does not exceed Rs 50 crore; and

Net turnover does not exceed Rs 250 crores.

It is difficult for a buyer to assess the category of a supplier, therefore he should ask for Udyam Certificate and rely on the category prescribed therein. Importantly, only micro and small enterprises are considered suppliers for the purpose of Section 43B(h). Medium enterprises are not regarded as suppliers and are not entitled to enforce prompt payment and interest for delayed payment.

MSMED Act, 2006 provides that the buyer of the goods or services should make payment within 15 days of delivery of those goods, if there is no written agreement between the two and in case there is a written agreement the payment should be made within 45 days or earlier even if the written credit period exceeds 45 days.In case some objection is raised by the buyer upon receipt of goods the same shall be intimated to the seller in writing within 15 days of receipt of such goods and in that scenario the payment should be made within 15/45 days as the case may be, from the day such objection is removed by the seller. It is further provided in MSMED, Act 2006 that if the payment against purchase of goods/services is not paid within the prescribed time then the buyer shall pay interest three times the bank rate notified by Reserve Bank, compounded at monthly rests for the default period. These provisions already existed in MSMED, Act 2006, however amendment in the Income Tax Act for the effective implementation of these MSMED Act provisions has gained attention apart from serious ramifications. Therefore, if MSMED Act provisions are not complied in case of payments to micro and small enterprise then;

(i) The buyer has to provide interest three times the notified bank rate compounded at monthly intervals as per the MSMED Act.

(ii) Section 23 of the MSMED Act states that interest paid by a buyer for delayed payments is not deductible under the IT Act. Thus, a buyer shall not get the expenditure of this interest from his income, despite providing for this liability.

(iii) The buyer shall not even get the expenditure of such purchase of goods/service if the payments are not actually made in prescribed time as discussed above.

(iv) In case the amount outstanding at the end of financial year is paid in the next year beyond the allowed time of 15 days/45 days as the case may be, shall be disallowed and added to income of the assessee, however the same shall be allowed in the year of payment.

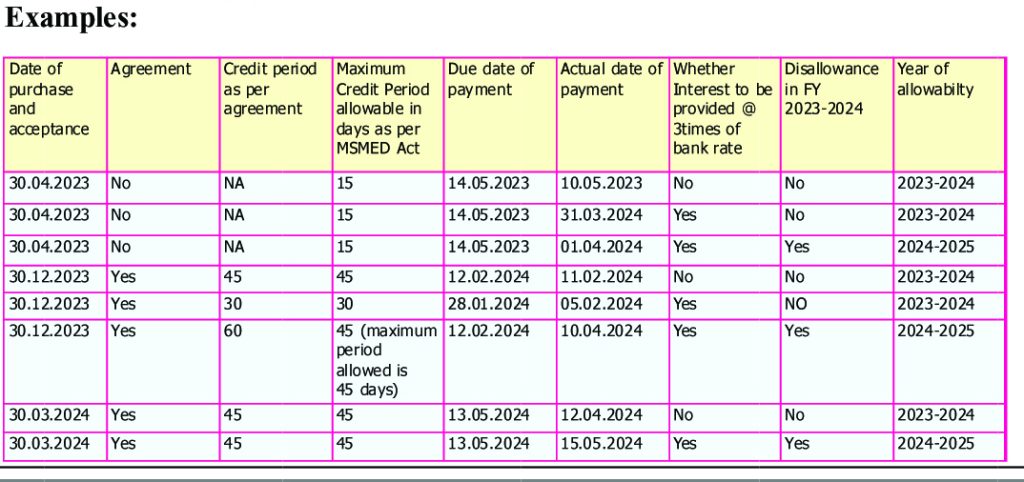

Examples:

The above provisions shall not apply to:

(i) Non registered enterprises under MSMED Act, 2006. Therefore, buyer should either ask for Udhyam Certificate or the declaration to the effect that the supplier is not registered under the MSMED Act,2006.

Search for Udyam Registration Number on the Udyam Portal under the newly enabled “Verify Udyam Registration Number” can be made at the following link

https://udyamregistration.gov.in/udyam_verify.aspx

(ii) Opening Payables outstanding as on 01.04.2023.

(iii) Traders whether registered or not, as the definition of enterprise under the MSMED Act only includes manufacturers and service providers and not the traders. It is just that vide Office Memorandum: No. 5/2(2)/2020/E/P&G/POLICY dated 2-7-2021 issued by Central Government traders are allowed to be registered on Udyam Registration Portal to avail benefits of retail and wholesale trade for Priority Sector Lending only.

(iv) Presumptive taxation scheme under the Income Tax Act like 44AD, 44ADA etc.

(v) Charitable trusts exempt under The Income Tax Act.

(vi) Capital expenditure. Further, depreciation can also not be disallowed on such capital expenditure.

The lawmakers have all good intention that insertion of clause (h) to section 43B of the Income Tax Act shall act as a supplement to the existing provisions under the MSMED, Act, whereby small and micro sector shall come out of liquidity crunch and shall get prompt payments., however this intended boon may probably become a bane as under:

(i) The buyers may try to shift their purchases from micro/small enterprise to medium and large sellers;

(ii) The micro and small enterprises may in fear of losing business opt out for registration with MSMED Act, thus loosing benefits under the said Act and priority sector lending assistances;

(iii) As these provisions are only applicable to manufacturers and service providers and not to the traders, thus it vitiates level playing field and may lead to enhanced working capital requirements of a trader and probably leads to unviability.

Example: Mr.A a wholesale trader buys from a manufacturer Mr.B who falls under micro/small category and sells to a retailer Mr.C, now Mr.C is not bound with the prescribed timelines of payment discussed above as Mr.A is a trader, however if Mr.A does not make payment to Mr.B in time his delayed payments shall get added to his income.

(iv) There may be a genuine case where payments of a buyer are stuck, (for e.g if he is a government supplier payments are usually delayed because of formalities, shortage of funds with treasuries etc) and he is not able to further make payment to his suppliers, in that case his purchases shall get added to income leading to unjustified and incollectable demands which may not be the intention of the law makers.

Example: Buyer’s usual net profit is say 5% of the turnover and the turnover this year is Rs.2 cr

Returned income: Rs.10,00,000

Say, tax paid thereon @30%(or applicable tax): Rs.3,00,000

Addition of delayed payment of purchases: Rs. 50,00,000

Additional tax on this disallowance: Rs.15,00,000

Thus, this may lead to unjustified tax liability in a particular year and material variation in taxable return of a person as the deduction shall be allowed on payment basis. Question arises that should the law be so stringent which not only is taxing buyer’s income but also the total expenditure itself ? Here the maximum profit is only 5% but the buyer is getting taxed on 100% of delayed payment of purchase

This amendment needs a revisit to achieve the real purpose and to avoid genuine hardship to the tax payer.